The September jobs report exceeded expectations with the addition of 336,000 jobs last month, nearly double the amount anticipated on Wall Street.

Add that ‘goldilocks’ figure to minimal wage inflation, and the scene is set for a soft landing for the economy, says Wedbush’s Daniel Ives, a 5-star analyst rated in the top 2% of the Street’s stock pros. This, in turn, is great news for the tech sector. In fact, with earnings season about to kick off, Ives thinks Wall Street is poised to be caught off-guard by the strength of reporting, laying the groundwork for a big end-of-year surge.

“Our view is that 3Q earnings over the coming weeks will be an eye-opener for the Street, as the transformational AI growth and stabilizing IT spending environment will create a massive tech rally heading into year-end, during which we expect tech stocks to be up another 12%-15% in 4Q,” Ives opined.

While Ives acknowledges that bears may try to temper the bulls’ enthusiasm, his advice remains clear: Ignore the noise and direct your attention towards the potential of this generational AI growth, with $1 trillion in tech spending anticipated on the horizon over the next decade.

With the prospect of all this about to take place, Ives believes certain names are well-positioned to gain, and we decided to take a closer look at some of his picks. Do these equities receive support from the rest of the Street? According to the TipRanks database, they certainly do; both are rated as ‘Strong Buys’ by the analyst consensus. Let’s see what makes them so.

Progress Software (PRGS)

We’ll start with a leading American infrastructure software company, the aptly titled Progress Software. This firm specializes in providing a wide range of software tools and solutions to help businesses enhance their operational efficiency and accelerate digital transformation. Since being founded in 1981, Progress has established itself as a trusted partner for enterprises seeking to harness the power of data and applications in an evolving digital landscape.

The company’s product portfolio includes a variety of software platforms, such as Progress OpenEdge, which enables the development of robust, scalable business applications, and Progress Telerik, a suite of developer tools for building modern web and mobile applications.

Progress’ customer roster is notably extensive, encompassing a diverse array of prominent clients, including Meta, Microsoft, IBM, Barclays, and S&P Global.

All the above helped the company deliver a strong fiscal Q3 report (August quarter). Revenue climbed by 15.7% year-over-year to $175 million, beating the Street’s forecast by $1.9 million. Adj. EPS of $1.08 also exceeded expectations by $0.08.

The company also delivered a net retention rate – a key software metric – above 100% and is actively seeking out its next M&A transaction. Earlier in the year, the company closed the $355 million acquisition of the document-oriented database operator MarkLogic.

For Daniel Ives, the prospect of more such activity is enticing and should further cement its standing in the space.

“The company continues to maintain an accretive M&A strategy as this environment now provides an attractive opportunity for PRGS to capitalize on a diminished valuation marketplace with $138.0 million in cash to spend on undervalued assets coming to market,” Ives explained. “We maintain our bullish stance on Progress as the company improves its cost structure while positioning to capitalize on growing demand for its entire product portfolio while maintaining an accretive inorganic growth strategy.”

These comments form the basis for Ives’ Outperform (i.e., Buy) rating on PRGS, while his $65 price target makes room for 12-month returns of 23%. (To watch Ives’ track record, click here)

In general, other analysts echo Ives’ sentiment. 3 Buys and 1 Hold add up to a Strong Buy consensus rating. Based on the average price target of $63.75, the upside potential comes in at ~21%. (See PRGS stock forecast)

Microsoft (MSFT)

If we’re talking about tech and how companies stand to gain from the AI revolution, then not much digging is required to get to one of the firms that stands to benefit the most. Microsoft has been at the forefront of tech’s rise, has played a pivotal role in shaping the modern technology landscape, and only Apple ranks higher on the list of the world’s most valuable companies.

Its ubiquitous Windows operating system is used by billions of computers worldwide, and it also offers a wide range of software applications and services, including the Microsoft Office suite, Azure cloud computing platform, and the Xbox gaming console.

Microsoft is also betting big on AI. It is heavily invested in ChatGPT maker OpenAI and has already announced that Microsoft CoPilot – the AI assistant feature for Microsoft 365 applications – is set to become widely available for enterprise customers next month.

Its positioning in this burgeoning space has given investors plenty to cheer about this year, and as with other tech giants, Microsoft has enjoyed the spoils of 2023’s bull market (up by 38%), even if its fiscal fourth quarter of 2023 (June quarter) report failed to entirely please.

On the face of it, there was little to worry about. Revenues reached $56.2 billion, representing an 8.3% year-over-year uptick and beating the consensus estimate by $710 million. Likewise, EPS of $2.69 came in ahead of the $2.55 anticipated on Wall Street.

However, along with Cloud service Azure’s revenue showing some deceleration, for F1Q, the company guided for revenues between $53.8 billion to $54.8 billion, which is at the midpoint, lower than the $54.94 billion the Street was hoping for.

While Ives is cognizant of the worries regarding growth, all signs are that there is little need for concern, especially with the anticipated AI windfall about to take place.

“Since Microsoft reported its June quarter investors have been in a ‘wait and see’ mode on the cloud growth trajectory of Redmond and most importantly when the AI monetization opportunity will start to show up in numbers,” Ives said. “We believe while management has talked about a ‘gradual ramp’ for AI monetization in FY24 we believe so far the adoption curve is happening quicker than expected based on our recent checks. Our latest Azure checks also show a clear uptick in activity sequentially (AI driven) which gives us further confidence in Microsoft exceeding its 25%-26% Azure growth guidance in FY1Q.”

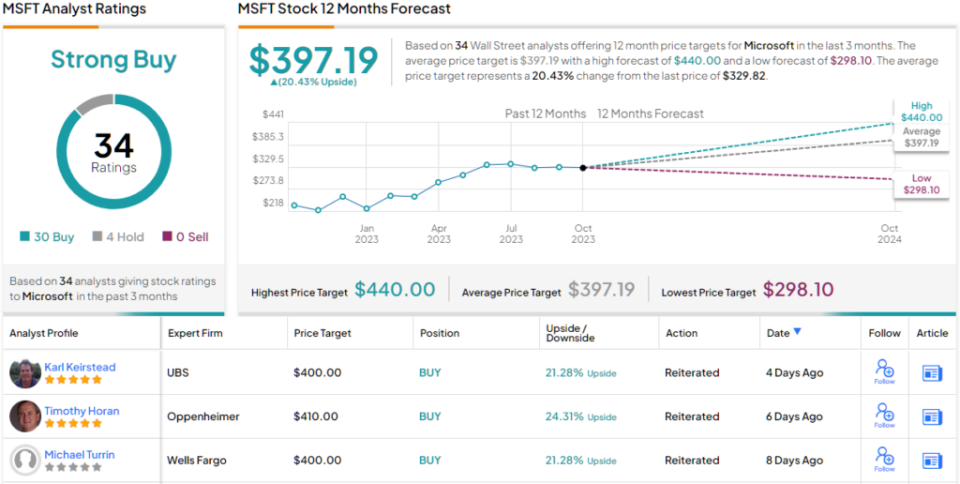

Conveying his confidence, Ives rates MSFT shares as Outperform (i.e. Buy) backed by a $400 price target, suggesting the stock will post growth of 21% over the one-year timeframe.

Overall, MSFT gets a Strong Buy consensus rating, based on a mix of 30 Buys against 4 Holds. The average target is almost identical to Ives’ objective, and at $397.19 allows for share gains of 20% over the coming months. (See Microsoft stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.