A smart investor is a patient investor, in the game for the long haul. Warren Buffett, a legend in the markets, has long been known for advocating long-term holdings – and so does the banking giant Morgan Stanley. The bank’s annual ‘Vintage Values’ report points out the firm’s top stocks for a ‘buy-and-hold’ strategy on the one-year horizon.

The current Vintage Values list has a lot to say on the subject, but a few features of their picks stand out. First, all of their choices are mid- or large-cap stocks. Second, their Vintage Values selections lean strongly towards high-quality names. And finally, these names are trading at a bargain compared to the market.

There’s one more important point to make about Morgan Stanley’s Vintage Value list. Since they started publishing these picks 14 years ago, the list has tended to outperform the S&P 500. The 2022-2023 list, the predecessor of this one, beat the index by 941 basis points over 12 months.

So let’s see just what Morgan Stanley says investors should buy and hold. Here are two of the firm’s Vintage Values.

NextEra Energy, Inc. (NEE)

The first Vintage Value pick we’re looking at is NextEra, a renewable energy company and an important component of the clean energy industry. NextEra has between $85 billion and $95 billion in infrastructure improvements planned for the next two years, and has 67 gigawatts of power generation in operation. NextEra is the owner of the Florida Power & Light company, the largest electric utility in the US, and provides power to more than 12 million people across the state of Florida.

In addition to its Florida operations, NextEra has assets in several other states, including emission-free nuclear power generation in Wisconsin and New Hampshire. The company is a leader in wind and solar power generation, and operates multiple renewable power generation facilities in Texas.

All of that is good, but NextEra sees the future of power generation in the hydrogen energy sector. The company is working with US government agencies to develop and fund green hydrogen energy projects, and is investing up to $20 billion into hydrogen capital projects, with a goal to develop up to 15 gigawatts of renewable hydrogen power generation by 2026.

At the bottom line, the company’s revenues have been increasing in recent years. In the last quarterly report, for 2Q23, NextEra reported revenues of $7.35 billion, beating the estimates by $1.18 billion and increasing almost 42% year-over-year. The company’s bottom line, a non-GAAP EPS of 88 cents, was 6 cents per share better than had been expected.

All of this leads Morgan Stanley’s David Arcaro to an upbeat view of the company. The analyst writes, “We remain bullish given low earnings risk, continued strong renewables demand, improving supply chain backdrop, and green hydrogen upside… Hydrogen projects will require deep skill sets across several areas where NEE has advantages. We expect NEE to be a leader in the green hydrogen market regardless of the Treasury provisions.”

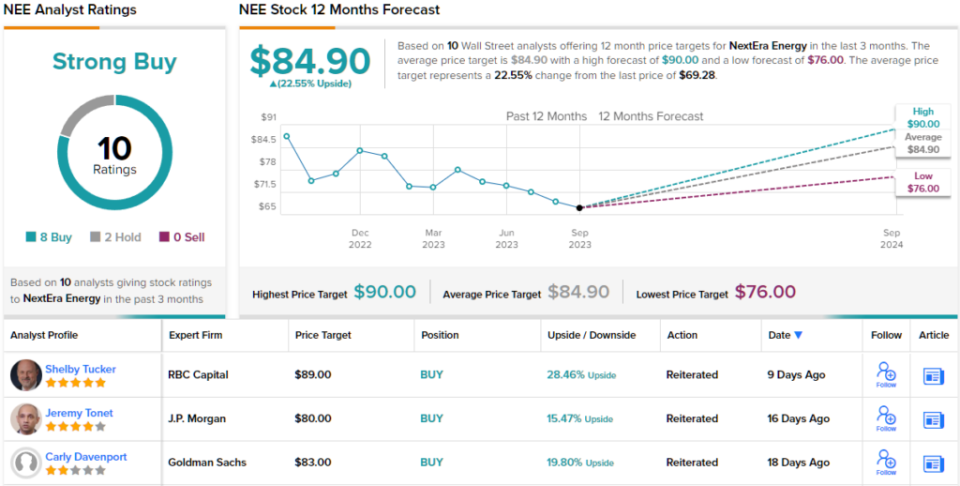

Arcaro’s comments back up his Overweight (i.e. Buy) rating on NEE, and his price target, now set at $90, suggests ~30% upside potential on the one-year timeline. (To watch Arcaro’s track record, click here)

Overall, this stock has attracted 10 recent reviews from the Street, with an 8 to 2 breakdown favoring Buys over Holds for a Strong Buy consensus rating. The shares’ $69.28 trading price and $84.90 average price target give the stock ~23% potential gain in the next 12 months. (See NextEra stock forecast)

Medtronic PLC (MDT)

The next stock we’ll look at from the Morgan Stanley Vintage Value list is Medtronic, a medical device company with a wide range of products targeting a variety of conditions. The company has a global footprint, and is a leader in healthcare technology, describing its mission as ‘attacking the most challenging health problems facing humanity.’

Some basic numbers will show the scale and reach of Medtronic’s operations. The company’s products have helped more than 74 million patients over the years, and looking forward, Medtronic has more than 210 active clinical trials testing out new devices and products. In its fiscal year 2023, which ended this past April, Medtronic reported making $2.7 billion worth of R&D investments, a solid indicator of confidence in its approach. And, of particular interest to return-minded investors, the company paid out $3.6 billion in dividends to its shareholders in fiscal year 2023.

The dividend is worth a closer look. Medtronic has already declared its dividend for fiscal 2Q24. The payment of 69 cents per common share marks a 1-cent increase from the year-ago quarter, and will annualize to 3.4%. The company has a dividend history stretching back to the 1970s.

Medtronic last reported earnings for Q1 of fiscal 2024, and showed a 4.5% year-over-year increase at the top line; the revenue figure of $7.7 billion beat the forecast by over $144 million. The company’s non-GAAP EPS, at $1.20 per share, was 9 cents better than expected. In a move that bodes well going forward, Medtronic also bumped up its earnings guidance, to the range of $5.08 to $5.16 per share, or a 7-cent increase at the midpoint. This compared favorably to the $5.05 consensus EPS guidance expectation.

Looking under the hood at this stock, Morgan Stanley’s Patrick Wood lays out multiple reasons for an upbeat outlook: “We see MDT’s pipe as well stocked from the innovation standpoint (e.g. Inceptiv, 780G, Simplera, Spyral, Micra, Pulse Select etc.), and gross margins are trending in the right direction with a c. 115bps beat despite heavy S&OP and supply chain work. Indeed, gross margin delivery back to c. 68% is worth c. 12% to group earnings alone, and we expect MDT to drive more consistent execution as it consolidates supply and manufacturing.”

“Trading on sub 15x calendar ’24 P/E, despite what we expect to be consistent MSD organic growth and potential c. 200bps upside to margins, along with less crowded positioning, we remain bullish on MDT shares,” Wood summed up.

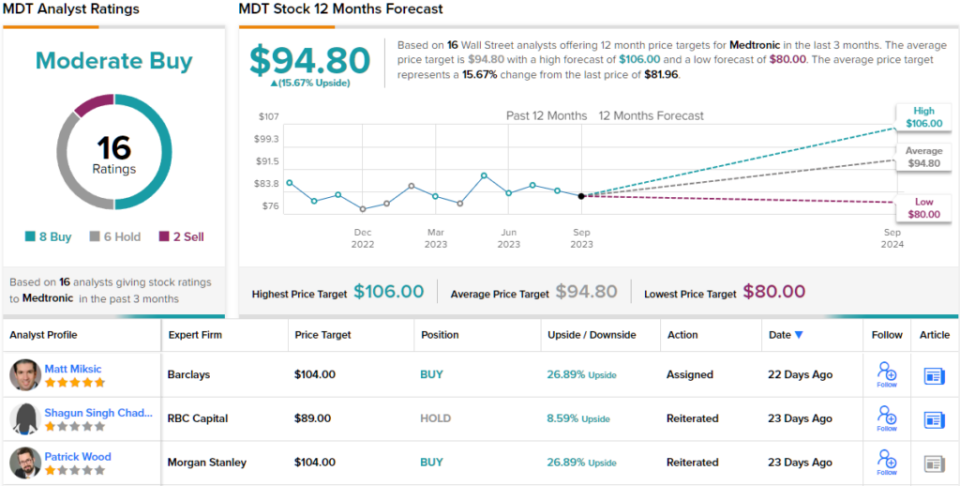

Bullish means an Overweight (i.e. Buy) rating, and a $104 price target that points toward a 27% one-year upside potential. (To watch Wood’s track record, click here)

Overall, Medtronic gets a Moderate Buy rating from the analyst consensus. The 16 recent analyst reviews include 8 Buys, 6 Holds, and 2 Sells, while the $94.80 average price target suggests ~16% increase from the current trading price of $81.96. (See MDT stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.